The current electronic component shortage primarily caused by MLCC’s continues to cause OEM’s serious problems and according to Industry Insiders, there is no end in sight to this problem (Ref:https://www.ttiinc.com/content/ttiinc/en/resources/marketeye/categories/passives/me-zogbi-20180302.html)

MLCC Shortages Are Creating Challenges In Multiple End-Markets in 2018

03/02/2018 // Dennis M. Zogbi in: Passives

Limited Capacity To Stack Ceramic Dielectric Will Extend MLCC Shortages To 2020 and beyond.

- Limited capacity expansion in the MLCC industry, specifically the ability to stack ceramic layers (limited capex in three-dimensional stacking capacity for barium titanate dielectric composition and nickel electrode paste) will extend shortages of MLCC to 2020 and beyond.

- As a result of expanding margins in ceramics- MLCC Manufacturers are NOT supporting low margin ceramic businesses, especially those that have exposure to precious metals such as ruthenium and palladium.

- MLCC are the Workhorse of the Electronic Components Industry. They are relied upon and used across multiple industries. In fact, because of the scientific principal governing electrical and electronic circuits, the requirement for capacitance and resistance is mandatory. The most cost effective solution had been and will continue to be for the next ten years the stacking of ceramic, but anywhere that other dielectrics can be employed will now grow as manufacturers have no choice but to distance themselves from such a tremendous reliance on barium titanate based ceramic dielectric. This will impact demand and capacity for other dielectrics, and force the development of next generation ultra-small component technologies that are based upon new processes (but familiar materials).

- The near-term process will be that customers will lose support in key segments; especially in consumer AV and home appliance where the added loss of a key MLCC vendors in Y5V dielectric has placed added pressure on prices.

- Any manufacturer with ceramic production capability will be targeted and rapidly approved as a vendor of capacitors in markets, especially automotive, where they have not supplied before. Competition for MLCC will become more pronounced because the high-tech supply chain only reacts when it is under intense pressure, and then it tends to overreact in the opposite direction.

Strategies for Managing Short Supply Scenarios

The traditional methods for addressing a parts shortage is to assume all manufacturers are the same and simply move down the supply base from tier one, to tier two, to tier three vendor levels and then target specific products that might be critical but unusual (high voltage, high temperature, NPO type) that may be sourced to smaller vendors in China, Singapore, Thailand, Malaysia, Slovenia, Hungary, Czech Republic, Japan, Australia, etc. The problem with this scenario is that everyone is already on this course of action as a viable strategy and capacity has already filled up in most of those areas do to the similar processes that buyers use to address problems like shortages of components. Some finance companies and manufacturers are already researching the raw material supply China’s in barium titanate, nickel, equipment, testing, to see who is best positioned to handle the coming shortages and who will benefit in FY 2020 as the market rushes to find alternative methods to produce MLCC and the PCB. From a Paumanok view, the very limited supply base and technology hurdles required to compete in high capacitance MLCC makes outside challengers a very limited threat because the supply chain for advanced engineered materials is even more limited and from the base in Japan supplies all the companies with captive BT and Ni powders.

Alternative methods outside the mainstream are already upon us in the form of thin and thick film integrated passive devices and integral passive substrates. This is the next generation of capacitance, resistance and inductance generation for volumetric efficiency and the next big area for passive component investment. The TDK investment in thin film barium strontium titanate production speaks volumes for the future, and Murata’s purchase of IPDIA points the way toward the next requirements for handset module manufacturers and wearables to generate power, connect and provide the capacitance and energy density needed to create advanced functionality and complete autonomous black box systems, be it a module, handset or automobile.

The Ultra-Small Case Size Content

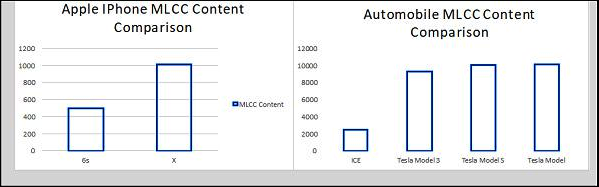

The following chart illustrates the adjustments to MLCC quantities by end-product market. So two key soft spots are in the increased capacitance requirements in handset and automobiles, which takes a significant jump upward as well move from the Apple 6s to the Apple X; and as we move from internal combustion engines to Electric Vehicles.

MLCC Content in Apple Phone and Tesla EV Migration

Source: KEMET Financial Presentation Feb 2018- ICE- Internal Combustion Engine- This trend is constantly upward and in motion. The content shifts upward inside handsets and cars will consume all the world’s stacking capacity. Real shortages will materialize as soon as the handset business begins to gobble up parts to satisfy internal shifts in black box requirements for capacitance.

What Paumanok is also pointing out in the above table is that there are similarities and overlap in the MLCC chain and the demand is focused on the high layer count, high capacitance MLCC in the X5R and X7R performance dielectric. These are stacked up to 1,000 layers to achieve the desired capacitance. Therefore, the capacity to stack ceramic is overwhelmed and the technology is so advanced in terms of manipulation of ceramic and metal nano-technology that the opportunity for the market to be overrun with competition is highly unlikely. MLCC manufacturers are all in excellent position to continue to benefit from this shortage of stacking capacity. It will also pull away the focus of these key ceramic capacitor manufacturers from any business segment or product line that is not as attractive as high capacitance MLCC, therefore, expect shortages in high voltage and high temperature capacitors and resistors that have constructions that expose them to the price of PGM metals (ruthenium and palladium).

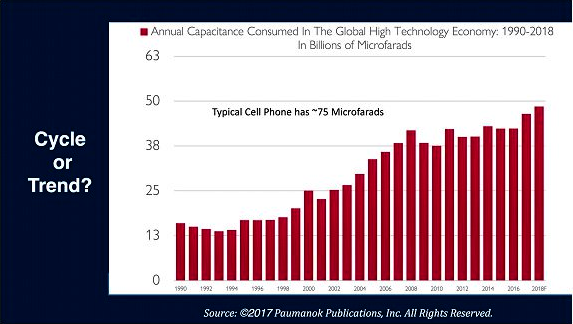

Capacitance Requirements per Person:

The following chart compares the volume of capacitors sold by capacitance value in microfarads to the global population to reveal that humans are requiring more capacitance each year. This can also be said of bandwidth and energy density and these three trends are important sign posts for investment.

Capacitance Requirement Trends Per Person

Source: Paumanok Publications, Inc.